By combining charitable intent with tax-advantaged lifetime income, a charitable gift annuity (CGA) can work very well for the right donor and for the right nonprofit. But a well-designed gift is only the beginning. Behind every CGA is a contractual payment obligation that a nonprofit must honor for the life of the annuitant, regardless of how markets perform or how the combined pool of CGAs managed by the charity evolves over time. That obligation deserves as much attention as the gift itself.

At Clifford Swan, we work with both sides of this equation. In addition to the wealth management services we provide to individuals and families, we advise and support charitable organizations on their planned giving programs, including investment management, administration, tax reporting, and ongoing monitoring of CGA pools, charitable remainder trusts (CRTs), and other planned giving vehicles. Conversations about CGAs have become more frequent lately, and for good reason.

Why CGAs Are Back in Focus

Charitable gift annuities are receiving renewed attention from donors, nonprofits, and advisors alike. Maximum payout rates published by the American Council on Gift Annuities (ACGA) have risen meaningfully in recent years, making CGAs more attractive to donors as an income-generating giving vehicle. Beginning in the 2023 tax year, the SECURE 2.0 Act created a valuable opportunity to fund CGAs through a one-time qualified charitable distribution (QCD) from an individual retirement account (IRA). That IRA-funded QCD counts toward the donor’s required minimum distribution, creating an income exclusion as opposed to a below-the-line charitable deduction; this is a meaningful benefit for those who would otherwise face a taxable withdrawal.

For donors seeking a combination of lifetime income and a lasting connection to a cause they care about, the current environment means CGAs are worth a closer look.

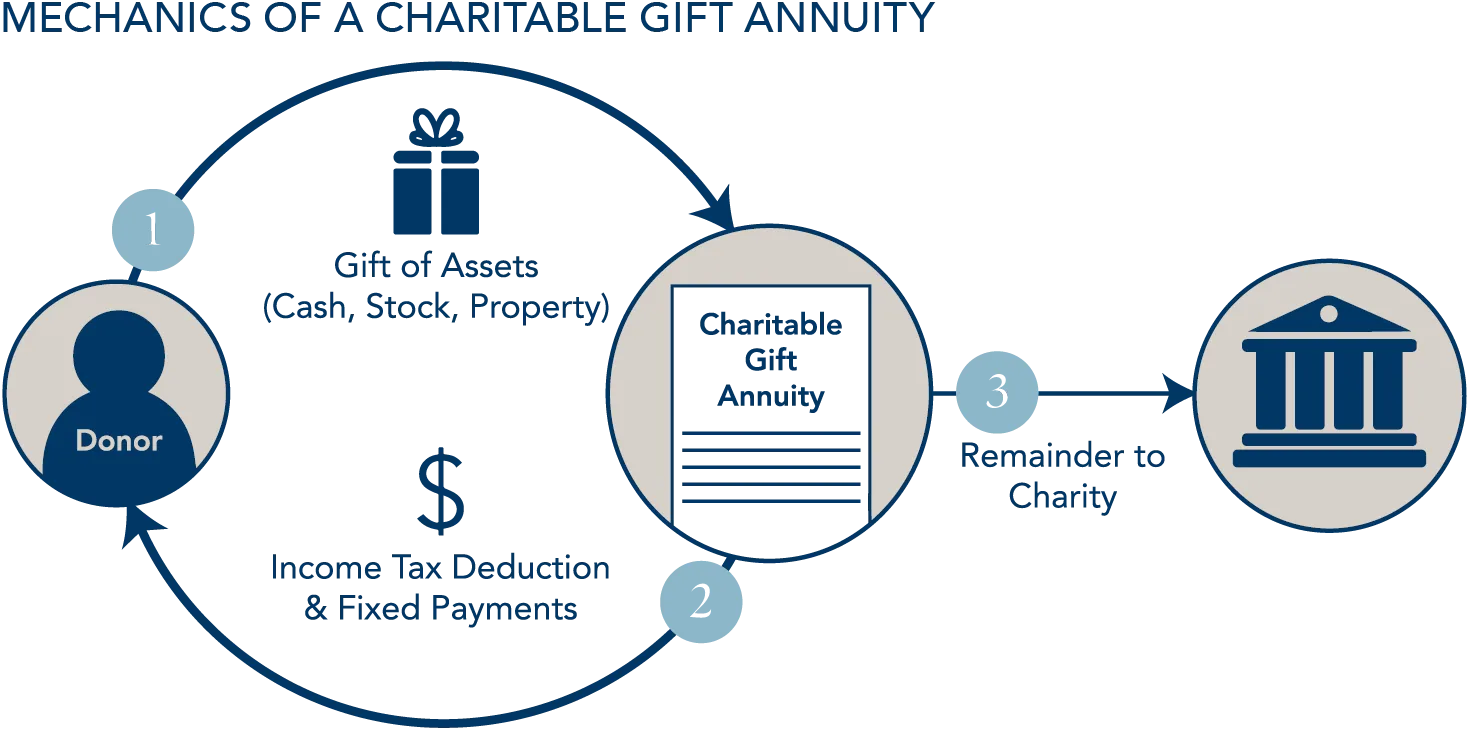

Simple Structure, Real Commitment

The basic structure of a CGA is straightforward. A donor makes an irrevocable transfer of assets (cash, securities, or other property) to a qualified 501(c)(3) charity. In return, the charity commits to making fixed payments for life to one or two annuitants, most often the donor(s). When the annuity obligation ends, the remaining assets support the organization’s mission. Most charities follow the payout rates recommended by the ACGA, which set a widely recognized benchmark.

When considering implementing a CGA program, the first question a nonprofit should ask is not, “How much can we raise through CGAs?” A better question is, “Can we commit to running a sustainable CGA program over the long term?” The most important consideration for nonprofit leaders is not the simplicity of a single CGA, but rather the contractual payment obligation created by each gift, and the added complexity that comes with managing a pool of them over time.

A prudently managed investment pool supports those obligations, but does not eliminate the risk. If CGA pool assets are diminished due to underperformance, long-lived annuitants, or prior gift terms that were too generous, the payments still need to go out.

What Strong CGA Programs Have in Common

Durable CGA programs tend to share a few characteristics worth understanding, whether you are a donor evaluating a charity’s stewardship or a nonprofit leader building or reviewing a program.

First, strong programs have clear, consistently applied gift acceptance guidelines. The organization knows what types of gifts it will accept, what it will avoid, and who has authority to approve exceptions. Discipline in this area protects both the donor and the organization.

Second, healthy programs maintain enough activity over time to allow for diversification by donor age, gift size, and payout rate. A CGA pool does not need to be huge to be well-run, but in a very small pool, a single long-lived annuitant, an unusually large gift, or an above-market payout rate can meaningfully skew results. New gift activity is what keeps a pool balanced and sustainable.

Finally, strong programs take administration seriously. Beneficiary records need to be accurate, payments made on schedule, and tax filings, state regulatory compliance, accounting, and recordkeeping handled reliably. Investment allocations should also reflect the expected payment horizon (duration) and liquidity needs of the pool. These behind-the-scenes tasks are central to sound stewardship of a donor’s gift.

Where CGA Pools Can Drift

Many struggling CGA pools do not begin as obvious problems. A pool is established, a few initial gifts are accepted, and payments go out on schedule. For a while, everything appears manageable. Over time, warning signs can quietly emerge: few new gifts coming in, heavy concentration in one donor or age band, rising administrative costs, or gifts going underwater.

A CGA pool in runoff, meaning one that is paying out more than it is taking in, is not necessarily a failure. It may still honor its obligations effectively and wind down in an orderly way. But it is a decision point that deserves deliberate attention. Leadership should weigh whether to rebuild the program, tighten gift acceptance guidelines, seek outside administrative or investment support, or manage the remaining obligations toward a planned conclusion.

A Practical Framework for Evaluating a CGA Program

For nonprofit leaders, a few practical questions can clarify whether a CGA program is on solid footing. For donors, these same questions offer a useful lens for evaluating whether a charity is managing its planned giving commitments responsibly:

- Who owns the program after a gift is accepted, and is that ownership clearly defined across Development, Finance, and Operations?

- Are gift acceptance guidelines current, documented, and consistently applied?

- Is the age mix, gift size, and payout rate of the pool being monitored over time?

- Is the pool being replenished with new gifts, or slowly moving into runoff?

- Are payments, tax reporting, state filings, and recordkeeping handled reliably?

- Does the investment allocation reflect the duration and liquidity needs of the pool?

- Does the Board receive enough information to understand the program’s health?

- These are not only fundraising questions. They are governance, investment, and stewardship questions, and the answers matter to everyone with a stake in the promise being kept.

Building the Foundation

Our work in this area extends beyond traditional investment management. We advise charitable organizations on planned giving programs of all sizes, including CGA pools and charitable remainder trusts, providing investment management, payment processing, GAAP-compliant accounting, and required tax and regulatory filings. When asked, we also participate in conversations with donors to help ensure each gift is clearly understood and serves its intended purpose within a sustainable program. Whether an organization is considering launching a program, evaluating an existing pool, or simply needs hands-on support so their development team can stay focused on donor relationships, we help build and maintain the foundation their program depends on.

A CGA program is not just a means to fundraising. It is a long-term promise. When that promise is supported by clear policies, sound investment management, reliable administration, and consistent oversight, it can serve donors and nonprofits well for many years.

The above information is for educational purposes and should not be considered a recommendation or investment advice. Investing in securities can result in loss of capital. Past performance is no guarantee of future performance.